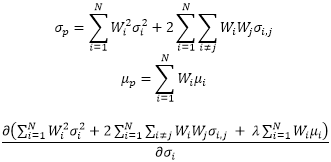

The maths behind the Hedgerow analysis is given below.

Where

- σp is the portfolio variance,

- Wi is the weight assigned to asset i,

- σi is the variance of asset i,

- σ(i,j) is the covariance of assets i and j,

- μp is the portfolio return,

- and μi is the average daily adjusted return for asset i.